https://www.infolink-group.com/en/solar/analysis-trends/Will-polysilicon-supply-shortage-ever-stop-this-year

Will polysilicon supply shortage ever stop this year

April 1, 2022 Albert Hsieh

- Share

Scan to share on WeChat

Will polysilicon supply shortage ever stop this year?

With countries setting net-zero emission targets for 2050-2060, renewable energy demand grows robustly. Amid energy transition trends, PV InfoLink expects global PV demand to surpass 230 GW this year. Strong demand is mainly sustained by China, which released several supportive policies last year, as well as energy transition-driven markets such as Europe and the U.S. In addition, Russia-Ukraine war accelerates Europe’s need to wean off its dependence on Russian fossil fuel, and thus demand for renewables looks strong in Europe.

In anticipation of a higher-than-expected demand, polysilicon supply will remain a major factor affecting prices across the supply chain this year.

Since the second half of 2020, polysilicon prices have been on the rise. Coupled with imbalanced capacity in the supply chain and China’s energy intensity control, polysilicon prices reached as high as RMB 270/kg (US$ 42/kg) in 2021. Fat profits drew existing and new players to expand thousands of tons of capacity. PV InfoLink estimated that polysilicon production will reach around 858,000 MT this year, which seems sufficient to supply 314 GW of modules. However, as it takes about six months for new polysilicon capacity to come fully online, real supply will not grow rapidly. Meanwhile, overcapacity in the wafer segment leads to higher-than-usual polysilicon inventory level. Against this backdrop, supply of polysilicon will remain tight throughout the year.

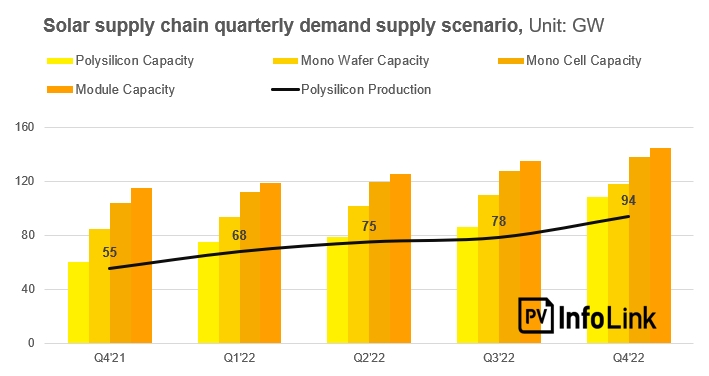

In addition to manufacturers that commissioned new lines in the second half of 2021, such as GCL, Yongxiang’s facility in Sichuan and Yunnan, and Daqo New Energy, many new lines will start production this year, including those of Yongxiang’s facility in Inner Mongolia, TBEA, and East Hope. Other manufacturers, such as Qinghai Lihao, Jingnuo New Energy, and CSG Holding, will also join the game. The chart shows that the real production will fall short of fulfilling demand from the downstream due to the time required for new lines to come online, despite rapid capacity expansion.

On the demand side, capacity expansion in the cell and module segments is continuing as leading manufacturers eliminated older capacity and raised shipment targets, but the pace has slowed due to shrinking profits amid overcapacity. It’s estimated that global cell and module capacity will grow by 31% and 26% YoY, respectively. The wafer segment, which has better profitability, will see continued large-scale capacity expansion, with the global total expecting to grow from 356 GW in 2021 to 476 GW this year, up 34% YoY.

With polysilicon supply unable to grow at a fast face, structural shortage in the supply chain will persist, if new polysilicon capacity couldn’t come online smoothly, while capacity expansion in the downstream continues. PV InfoLink projects that polysilicon prices are not likely to drop rapidly this year, with prices even going upwardly in the short term due to rising demand.

Once manufacturing activity on new polysilicon lines increases in the second half of the year, structural shortage will gradually ease, allowing polysilicon prices to decline. Having said that, prices will not decline rapidly in the second half as high season falls upon. So, prices may stay at above RMB 200/kg in the end of the year, with overall prices decreasing at a pace slower than earlier prediction. Polysilicon supply in regions outside of China, on the other hand, enjoys small premiums, for it can enter the U.S. market and has advantage of low carbon footprint.

Other factors affecting polysilicon supply are China’s policy on energy intensity and consumption and global trade barriers. Energy intensity controls imposed in the second half of 2021 forced many energy-intensive industries to cut production, especially raw material manufacturers such as polysilicon and silicon metal. Sharp reduction in production caused prices to surge, driving up costs across the supply chain. It’s expected that China will not impose such strict energy control this year, but if any, supply may be affected again and lead to large price fluctuations in the supply chain.

In terms of foreign trade barriers, the U.S.’ sanctions against goods from Xinjiang remains the biggest threat. Under the Act, products linked to Xinjiang supply chain could be detained by the U.S. Customs following the Withhold Release Order. The import ban will be implemented on June 21, 180 days after the effective date of the Act. The U.S. government has yet to release the standard for certificate of origin investigation; meanwhile, shipments of some manufacturers to the U.S. were seized due to the lack of complete documents. At present, using polysilicon outside of Xinjiang is the safest for the U.S. market. Currently in non-China regions, there are Wacker, OCI and Hemlock that can supply polysilicon, but they only account for 15% of the global total, which equals to 47.3 GW of module volume, enough to supply 30 GW of US demand this year. However, overseas polysilicon also supplies N-type wafer and low carbon footprint product manufacturers, thus making overseas polysilicon a key material for strategic planning of vertically integrated companies this year.

Despite continual additions of new polysilicon capacity, structural shortage will linger until new lines come fully online in the second half. By then, there will be bigger room for prices to fall. Developments in China’s energy intensity policy and foreign trade barriers should be monitored closely for they also determine whether the polysilicon segment will disrupt the PV supply chain this year.