https://pv-magazine-usa.com/2024/07/24/bigger-is-better-as-module-makers-power-ahead/

Bigger is better as module makers power ahead

Image: Longi

Share

From pv magazine print edition 6/24

pv magazine: Exawatt produces a quarterly module tracker report. What are you seeing in terms of power output trends?

Molly Morgan: For all technologies, we’ve seen an increase in power output from 2009 through 2023. All of the module releases have pushed for higher power. It’s almost alongside efficiency as the main selling point for manufacturers. We forecast module power out to the late 2020s and, in that, we see this trend continuing as old module series get retired and there is a push for newer, more advanced modules that come with higher module power.

In 2024, the modules that are continuing to improve on power output are tunnel oxide passivated contact (TOPCon), heterojunction, and back contact [devices]. And we’re expecting to see this improvement continue through to the end of the decade. By contrast, with the stagnant technologies like mono passivated emitter and rear contact (PERC), we’re not seeing efforts from manufacturers and the resulting improvements in efficiency. We don’t expect to see module power improvement as the technology becomes less relevant.

And is your analysis that there is still a lot of headroom for TOPCon, heterojunction, and back contact?

We forecast that the average power output will keep continuing to improve but, in saying that, the big jump in module power historically has really been the big increase in wafer size across all technologies. With the adoption of G12 and M10 wafers, we see modules using these wafer formats win when it comes to power output.

So are you saying that the switch to larger wafer sizes has an outsized impact on module power output?

That’s right. Just by switching to the larger wafer size, manufacturers have been able to jump the equivalent of a technology progression, in terms of power.

Speaking of technology progression, the big switch now is toward negatively-doped, “n-type” cells. Are you seeing new mono PERC or other, positively-doped “p-type” modules coming onto the market?

We’re currently in the process of going through the latest round of data collection for the latest PV module tracker report and what we’ve been seeing is module manufacturers no longer promoting their mono PERC products, and even removing them entirely from their websites over the last year or 18 months. This is to make room for the n-type offerings. I think this is a significant “nail in the coffin” for mono PERC.

On a manufacturing basis, do you believe those mono PERC lines are now being retired?

That’s a good question. It’s hard to tell whether mono PERC lines are being kept idle or being upgraded. Although in saying that, some manufacturers are quite keen to announce that they are upgrading lines from mono PERC to TOPCon. But given the vast amount of overcapacity, I don’t know if the information from a handful of manufacturers means that it is an indication of what is happening across the industry.

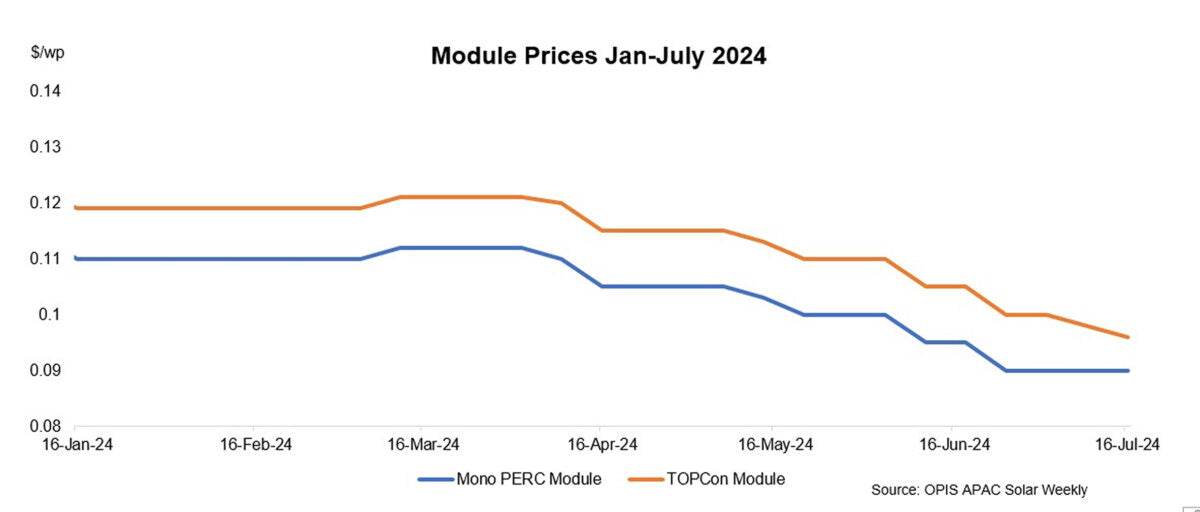

What is your understanding of TOPCon, when it comes to cost?

The transition to TOPCon has been encouraged and reinforced by it having achieved cost parity with mono PERC. TOPCon is set to have the lowest manufacturing cost per watt. It is hard to imagine what could knock TOPCon off its throne, in the very near future at least.

It has been a rapid transition but not unexpected when you look at the underlying cost dynamics. As there is a better module that can be produced at the same or lower cost, it is not surprising that TOPCon has been able to become dominant in terms of market share.

You mentioned the increase in cell sizes and its impact on power output. This has also led to far bigger modules. What are you seeing lately in terms of module dimensions?

In our dataset we can see the switch to larger wafers take hold and then plateau as the standardization of wafer dimensions, in late 2023, took force. We see quite a clear cut off from the rapid increase in larger wafers, and then it settling.

The average module area across our whole dataset stopped rapidly increasing also, at around 2.35 m². We definitely don’t expect to see a big jump up to larger sizes now that a standardization of sizes has been put in place and everyone has stopped competing in that sense.

So the standardization appears to have had an impact and manufacturers are sticking to what they agreed?

It does, and that’s always nice. It does look like the standardization, the agreement, has fully fed through to what we see in the data. And this will provide some relief to the installation segment. I can finally tell installers, “I have some good news for you.”

Author: Molly Morgan oversees Exawatt’s tracking and forecasting of PV module efficiency and architecture. She also undertakes analysis of capacity, production, and financial data for PV manufacturers. Morgan joins the pv magazine Awards jury, in the modules category, for the second time, in 2024.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.